5 reasons I Favor Junior Exploration Companies

I started following Gold and precious metals in 2002 and first invested in small cap and junior resource companies in 2005. Until recently I always focused on junior producers rather than junior explorers. Production stories were easier for me to understand. Towards the end of the 2008-2011 bull cycle I began covering more exploration companies and by late 2016 my focus had almost shifted entirely to exploration companies. In this piece I discuss the reasons why I currently favor junior exploration companies.

Exploration Companies From This Point Offer Greater Upside Potential

From the very bottom or from around the start of bull markets producers are the best buy for two reasons. First, producers make huge moves off the bottom. In studying bull and bear markets in gold stocks I’ve noticed that producers not only make huge moves off the bottom but a good deal of their upside during a bull market is captured during that initial move.

From late 2000 through 2003 the HUI gained 640% but from the 2005 low to the 2008 peak it only gained 213%.

I looked at eight producers in the GDXJ (with a median market capitalization of roughly $1 Billion) and measured their performance from their 2015-2016 low to 2016 peak. The average gain was 314%. For this group to rise another 314% we would probably need to see Gold retest its all time high. That would require much more time than the roughly nine months to one year required for the initial rebound.

Secondly, exploration companies as a group tend to lag the sector until a turn has been confirmed. Individual explorers can certainly make huge percentage moves off the bottom but as a group more value is found in explorers after the initial surge.

Exploration Companies Can Be Less Dependent On Rising Metals Prices

Once metals prices have bottomed and the cycle has turned, exploration companies don’t necessarily require rising metals prices to be successful. If a junior explorer has made a discovery that could be economic at $1100-$1150 Gold, then it doesn’t require Gold to consistently rise in order to create value. That junior can add value by growing its discovery through more drilling or it can add value by de-risking the project and moving it closer to production. If metals prices are not rising then a producer needs to grow its production or grow its resources and reserves to add more value. It’s very difficult for a producer to do that considering most of its capital would go into the mine.

We should note a new bull cycle is important for exploration companies. During a bear market, only the absolute highest margin deposits are sought after. Exploration is cut back and capital for the junior sector is scarce. Junior explorers are extremely reliant on a bull cycle. They need it to be in place but from there don’t necessarily need metals prices to shoot to the moon.

The Big Money is Made in Exploration

A big investor in the junior sector recently told me this. He noted that most of the big names in the industry earned their wealth in exploration and not production. The road to riches in this industry is more attainable through exploration than through an actual mining company.

Individual Investors Have an Advantage

There are a few reasons for this. First, it is very difficult for the big money to get involved in junior explorers. They are often stuck with buying positions in majors or in GDX and GDXJ. Institutions that do invest in juniors cannot do so in the open market. They have to do it via financings.

Second, because there are so many more exploration companies to choose from (relative to producers) it is easier for an individual investor to gain an advantage. While analyst firms in Canada do cover juniors, they cover producers but few microcaps or nanocaps. That leaves an opportunity for individuals who through extensive due diligence can find low risk and neglected opportunities.

This is also true of the entire junior sector but individual investors have a much better ability to get in and out of positions. When an institution takes a position in a junior they have to hold it indefinitely.

Industry Fundamentals Strongly Favor Junior Exploration Companies

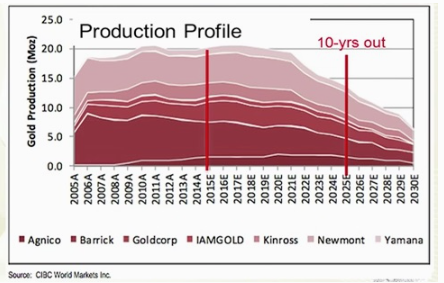

We saved the best and most obvious reason for last. It is well known and well reported that the pipelines of major producers are dwindling and need to be replenished. Production pipelines for major producers are set to fall off a cliff after 2021. Take a look at this chart from CIBC World Markets.

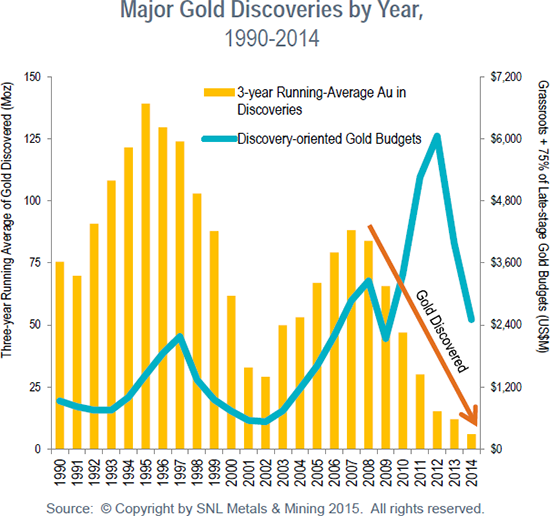

Moreover, fewer and fewer discoveries have been made in recent years even amid record exploration-oriented spending.

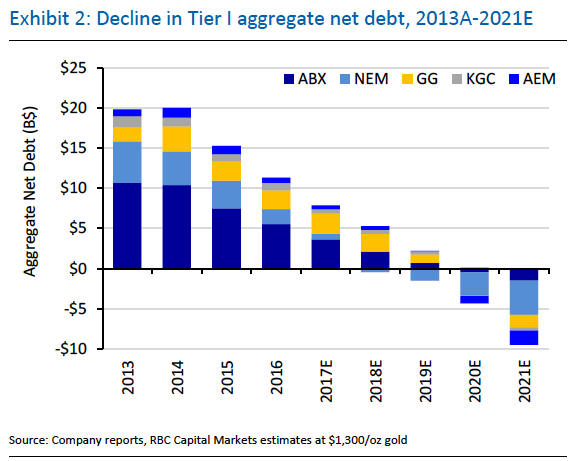

Several years ago the major mining companies were in survival mode and in no position to acquire. However as the primary trend has turned the majors have cleaned up their balance sheets and are in a stronger position to be able to acquire.

Over the next few years we expect the majors will be quite active in investing in and ultimately acquiring the juniors that have discovered and are developing gold deposits with high margin potential. Since 2015 the M&A activity has revolved around producers and producing assets. There are only so many of these to go around and that is why the majors have migrated down the food chain and have taken equity stakes in junior exploration companies. The next step could see majors acquiring companies that are in the advanced stages of exploration, rather than development.

Investing in junior exploration companies is very risky but I have shifted my focus to this group because of the backdrop of a bull market, strong industry fundamentals and the best risk versus reward potential (compared to other companies). This is why I’m seeking out and investing in the junior exploration companies that 1) are advancing deposits with high margin and multi-million ounce potential or 2) have earlier stage projects with potential to become high margin and multi million ounce deposits. In a future article I will discuss the criteria I follow when seeking out junior exploration companies. For professional guidance in investing in this sector consider learning more about our premium service including our current favorite junior exploration companies.

Jordan Roy-Byrne, CMT, MFTA