Obama Kills Osama After the Bernank Spoke, US Dollar Bubble Bursts Trending Towards USD69

What a week! A series ever more historic events accompanied by the dollar’s continuing in the background meltdown.

What a week! A series ever more historic events accompanied by the dollar’s continuing in the background meltdown.

Firstly, the Bernank spoke, spouting more central bank propaganda which as expected has been liberally lapped up by the mainstream financial press and further regurgitated at length by the BlogosFear, after all talk is cheap when compared with the increasing costs of actually doing something.

The facts are that the vast majority of academics and financial press talking heads have been wrong on QE since it started in March 2009, who recently with the benefit of hindsight have been stating that the rally in stocks and commodities has been purely as a consequence of QE1 and QE2, despite the fact that many of these same commentators had during 2009 been stating that QE would NOT be able to prevent DEFLATION and stocks and commodities would FALL as a consequence of what amounts to perma deflation propaganda, additionally many had stated during early 2010 that QE had come to an END and that there would be NO QE2 (Google their name + QE 2009 / 2010).

Of late many of these deflationistas’ have been attempting to reinvent themselves with the benefit of hindsight of a 100% run up in stock prices that they have not only missed but have been actively advocating the betting against to recognise aspects of the Inflation Mega-trend in a luke warm manner as they are in unable to abandon the red herring theory of debt deleveraging deflation as I warned of right at the start of the current phase of the Inflation Mega-Trend in November 2009 (18 Nov 2009 – Deflationists Are WRONG, Prepare for the INFLATION Mega-Trend ).

Why do deflationists have it wrong ?

It is that focusing on the deleveraging of the the debt mountain is a red herring, taken on its own then yes it DOES imply deflation as the debt bubble ‘should’ contract. But given the asset price reaction of 2009 that is NOT what is actually taking place! the Debt bubble is NOT deleveraging, the bad debts are being dumped onto the tax payers! The huge derivatives positions that act as the icebergs under the ocean as compared to the asset price tips that we see above water are not contracting but expanding!

The actual reality of the so called great deflation of the past 2-3 years is revealed by the below graph for US CPI inflation that makes a mockery of such deflation commentary that amounts to nothing more than perpetuating central bank propaganda.

And don’t forget that real inflation is probably between 50% and 100% higher than the official inflation rate as my research on UK inflation has revealed, which would lift the current U.S. official CPI inflation rate of 2.7% to between 4% and 5.4% as more reflective of the general populations actual inflation experience.

Bernanke’s Latest Deflation Propaganda Money Printing Speech

Prior to the speech there was much speculation from the talking heads that Bernanke would be announcing an end to QE2, my view on QE money printing has remained constant for several years now in that once overt money printing starts it cannot end whilst large budget deficits persist which means that QE3 will soon follow the scheduled end of QE2 in June. The strategy remains for the central bank to play its part in inflating public debt away by means of high real inflation that erodes purchasing power of wages and lifetime accumulated savings and wealth as covered at length by the 100 page Inflation Mega-Trend Ebook of January 2010 (FREE DOWNLOAD).

Therefore I expected Bernanke to continue to pump out deflation propaganda such as focusing on core inflation that excludes food and energy costs because off course everyone has stopped feeding and heating themselves, so as to allow the Fed to continue with the stealth debt default of US Debt by means of high real inflation. As I have stated several times during the past few years, IGNORE central bank propaganda statements on QE ending, or not continuing because it is a LIE, there WILL be QE3, no matter what the Fed says as the Fed statements are nothing more than economic propaganda focused on managing the general populations inflation expectations.

The facts are that QE3 has effectively already begun! One only needs to look at the series of ever more desperate money printing announcements coming out of Japan to see what lies in store for the U.S., as the default fall back position in the face of any financial or economic adversity is for every central bank to press the print money button, where QE is just one manifestation of.

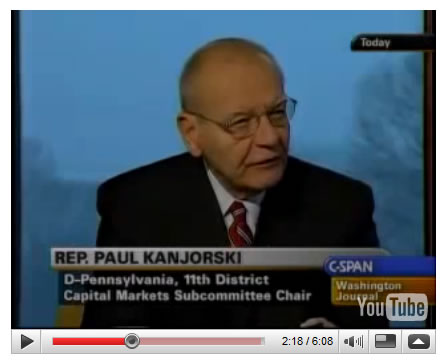

The bottom line where the markets are concerned is that QE has always been one element that is driving the bull markets in stocks and commodities because the whole system is geared towards incentivising people and investors to spend and speculate rather than save as the alternative is financial armageddon, which is something that all central banks remain petrified of, and therefore anything, including 10% real inflation rate is better than total economic collapse that would fast follow a collapse of the bankrupt banking system as nearly occurred during September 2008 as the following video illustrates just how close the U.S. financial system came towards total collapse ( Excerpted from the Interest Rate Mega-Trend Ebook – FREE DOWNLOAD). At 2 minutes, 20 seconds into this C-Span video clip, Rep. Paul Kanjorski of Pennsylvania in February 2009 explains how the Federal Reserve told Congress members about a “tremendous draw-down of money market accounts in the United States, to the tune of $550 billion dollars.” According to Kanjorski, this electronic transfer occurred over the period of an hour and threatened a further $5 trillion to be drawn out triggering a total collapse of the Financial System, which prompted Hank Paulson’s emergency $700 billion TARP bailout action.

Video Served by Youtube

Bernanke says he fears that QE3 will do more harm than good in terms of inflation, but as I wrote in the Stocks Stealth Bull Market Ebook, it’s too late, the harm has already been done with QE1 and QE2, the inflation time bomb is already going off, which is further enhanced as a consequence of the falling dollar.

The QE Bull / Bear Debate

Where the markets are concerned The QE debate boils down to two fundamentals positions of those that are riding and profiting from the stocks and commodities bull markets against those of perma-bear persuasion that not only consistently miss whole bull markets but give up all of any gains they may have made during preceding bear markets. This factor encompasses 99% of the debate that goes on across the Blogosfear. Now whilst some may conclude that it is a case of perma-bears arguing against perma-bulls, however that is not quite accurate for in a bull market Investors SHOULD be a BULL, likewise in a bear market, investors should be bears, because that is how one preserves and grows ones wealth and not by betting against EITHER bull or bear markets. Whilst Everyone now several years on with the benefit of hindsight recognises the importance of QE, though in simplistic and in herd like instincts elevated to exclusivity status when in actual fact it is just one of many possible HINDSIGHT reasons that can be used to explain market price action AFTER the fact much as I suggested would occur right at the birth of the stocks stealth bull market in mid March 2009 (15 Mar 2009 – Stealth Bull Market Follows Stocks Bear Market Bottom at Dow 6,470 ).

A. The markets move ahead of the economy, whilst I don’t profess to know the EXACT reasons of why they will move AHEAD until that becomes apparent AFTER the market has already moved, however I do have some reasoning in that INFLATION, Zero Interest Rates (Forcing savers / financial institutions to take risks) Quantitative Easing (money printing), and HUGE Fiscal stimulus packages that are laying all of the ground work for the next bubble regardless of how bad things appear as any outcome that prevents another Great Depression will be seen as bullish! i.e. even a low growth high inflation stagflationary environment WILL be seen as a positive outcome against the present day data that points to a collapse of global demand on a scale not seen since the Great Depression. The governments HAVE learned the lessons from the Great Depression and WILL succeed in inflating the asset prices and ignite the next perhaps even bigger bubble, meanwhile the stealth bull market will continue which by the time everyone realizes what’s going on stocks will already by up by perhaps more than 50% from the low.

More on QE as excerpted from the recent Stocks Stealth Bull Market Ebook Download Now-(PDF 2.8meg), the only requirement is a valid email address.

Quantitative Easing AKA Money Printing

U.S. politicians are living in fantasy land where they think they can get away with printing money and debasing the dollar without any consequences, they either do not care because they have become rich on the cash funneled to them by their bankster masters who they serve, or that they are delusional, completely detached from the real world. Many countries in the past thought the same, Germany, Russia, Italy, Zimbabwe to name a few and they ALL economically collapsed leaving the holders of their currencies with worthless paper to sell on ebay as high denomination trinkets, though off course the US dollar has already lost over 90% of its value during the past 100 years as a consequence of the stealth debt default through Inflation.

The stealth theft of wealth by means of high real inflation has been getting another accelerant these past 2 years ( in addition to public debt and POMO) in the form of direct money printing (electronic) by the US Fed to the tune of $2.3 trillion to first buy mortgage backed securities and then monetize the U.S. budget deficit that comes in at an annual $1.5 trillion and likely to continue at approx 1.5 trillion a year for a decade, that requires direct purchases by the Fed because no one else is dumb enough to buy the literal flood of paper, in fact now over 70% of new debt issuance is purchased by the Fed with most of the rest by other money printing central banks.

Whilst $2.3 trillion may not sound like a lot given the size of the approx $15 trillion annual GDP U.S. economy, but we are living in a fiat currency world where fractional reserve banking allows the banks to create credit at more than X10 the electronic print run and many, many times more during the pre-credit crisis credit boom. Where’s the money gone ? Well not much into loans to main street but it has into assets on leverage such as commodities and stocks and off course the Fed’s bankster brethren making over a trillion in risk free profits on buying US government backed bonds such as Treasuries and mortgage backed securities, U.S. tax payer funded profits without risk.

This is why the past year has seen virtually every analyst jump on board the QE bandwagon as a rear view mirror explanation for why stocks have soared, though backtrack to Feb / March 2009 and quite a number of these same so called analysts were explaining at length why QE meant that stocks would NOT RISE ! (Google it).

Worse still, a year into the stocks stealth bull market trend (March 2010) these same analysts were excitedly stipulating that the Fed had indicated that QE had come to an end and had started to unwind its positions and therefore implying that the so called bear market rally was over, following which along came the start of QE2 in November 2010, these same analysts are now suggesting that there will be no QE3. No wonder 90% of traders and many investors are on the losing end of trends because approx 95% of what they are reading is garbage pumped out by nothing more than sales men, academics, journalists or frankly media whores. The record is all there on Google to be confirmed within a minute or so. So as I say ALWAYS say, research each analysts past record before you pay any attention to their most recent diatribe. For it is always easy to pump out propaganda in support of ones pre-existing perma-view usually pushing sales but infinitely more difficult to arrive at a probable trend conclusion.

So whilst so called analysts had convinced themselves during early 2010 that QE had come to an end. However my conclusion has remained the same for over 2 years now that once Quantitative Easing starts it CANNOT END whilst large budget deficits exist regardless of what the central bankers publically state, as their focus is in massaging the expectations of the general population and financial markets with regards positive expectations on the economy and inflation and NOT in publicising accurate projections, as that would make their jobs much harder as I elaborated upon during mid 2010 (13 Aug 2010 – The Real Reason for Bank of England’s Worthless CPI Inflation Forecasts ).

The facts are and have remained for two years now that QE is INFLATIONARY (which is why I termed it as Quantitative Inflation in March 2009), which ultimately means HIGHER Commodity Prices ($ oil is not soaring just because of political unrest), Consumer Prices, Asset Prices and eventually Interest Rates (covered in the bonds section). Though it’s not just the U.S., ALL countries are at it, any economic problem and they press the print money button because it is far easier politically to print money (stealth theft of purchasing power) then to raise taxes / interest rates.

The whole point of QE money printing asset buying was to generate economic growth by means of boosting the wealth effect. What the central bankers such as the Fed and BoE never factored into their formulae’s was that their bankster brethren would use the cheap money to buy commodities on leverage rather than make loans to main street, hence sending asset and commodity prices soaring well beyond even the real inflation rates of between 7% and 9%, despite the fact that they did the exact same thing during mid 2008 to crude oil. Yes there is a wealth effect for the bankster’s and the few who have been able to bite the bullet and get on board the stocks stealth bull market and commodities, with prices being inflated by bankster’s courtesy of central bank easy money.

Inflation Time Bomb – Each QE builds up inflationary pressures in the U.S. economy that act as a ticking time bomb primed to go off, I cannot over state how inflationary QE is for an economy, even if QE stops at $2.3 trillion (which I doubt) then that pressure will remain, the ignition for it will probably ironically lie with rising short-term interest rates because QE induced near zero short rates have actually acted to suppress economic activity as the expanded Fed balance sheet has acted to soak up excess dollars and thus acted to suppress consumer price inflation whilst boosting asset price inflation, however as noted elsewhere in this ebook it is gradually leaking or flooding back into consumer price inflation via mechanisms such as foreign capital flows. At the end of the day QE of $2.3 trillion will eventually translate into new fiat currency money supply of between $20 trillion and $40 trillion, in a gradual process of inflation leakage as U.S. CPI that inexplicably to the mainstream financial press trends ever higher. Throw in several more QE’s and those numbers can be doubled yet again which illustrates the ticking inflation time bomb.

If for whatever reason the Fed takes fright to the inflation monster it has created and suspends QE at or near current levels then that still would require QE to be unwound to eliminate the inflation monster that would still be enough to send U.S. CPI soaring as short-term interest rates rose. The net effect would be for the US bond market to plunge or even crash taking the dollar down by several notches with it – ALL INFLATIONARY.

There really is no way out for the Fed, for if they continue QE its inflationary if they suspend QE and raise interest rates its still inflationary, hence Inflation is a ticking time bomb in the U.S. that WILL explode.

PIMCO – has reportedly dumped all of its U.S. Treasury Bonds, in response to the expected end of QE, the Blogosfear ran and cried panic for stocks and more importantly bonds to imply that there will be no more QE! – Well that’s not going to happen whilst large deficits exist that require the central bank (Fed) to monetize debt (buy government bonds). Instead, if Pimco and other bond funds are liquidating treasuries then where are they going to invest ? Yes I know they will likely hold a lot of cash as a stop gap, and apart from shorting treasuries which I have been advocating since August 2010, it seems obvious to me that instead of investing in bonds Pimco is going to invest in equities, as the always rear view mirror looking financial press will only see AFTER the fact – perhaps some 6 months down the road when perhaps the Dow has added on another 2k then the headlines will be PIMCO sold bonds to buy stocks !

Implication for stocks – Just as QE1 and QE2 were BULLISH (inflating asset prices) so will QE3 and after it QE4 that reinforces the primary bull market trend, for the U.S. will not stop printing money whilst the budget deficit remains anywhere near 10% of GDP (current approx 9%) and each time the U.S. announces another print run (QEx…) so it will imply ever higher future Inflation AND Interest Rates and so will weaken the U.S. Dollar (in relative terms because all fiat currencies are in free fall against one another), but not to worry asset prices are leveraged to real inflation courtesy of the likes of QE which means stocks should out perform loss of purchasing power.

In terms of market timing, weakness ahead of the end of QE2 in June and into the no mans land before the announcement of QE3.

So pay no attention to analysts / mainstream financial press and the Fed noises indicating an end to QE, instead keep your eye on the U.S. budget deficit as the most reliable indicator for future QE, and so I don’t see why I should change my view that QE will run for the whole decade as the U.S. follows Japan towards debt at 200% of GDP (monetized courtesy of the Fed), though probably QE9 will be the straw that breaks the camels back.

The U.S. Dollar Bubble Has Burst!

Whilst the mainstream press talking heads continue to talk about bubbles everywhere except the biggest bubble of all which is the U.S. Dollar, that partially manifests itself in the USD index trending lower, though given the fact that all currencies are in free fall against one another the dollar bubble bursting is more evident in soaring commodity prices that are leveraged to real inflation. The US government and central banks are accelerating the trend for the destruction of the worlds reserve currency something that is more than evident in the rush into Gold and Silver as alternative currencies to fiat paper because they cannot be printed and therefore more difficult for the master manipulators at the Fed to manipulate lower as they have done so for US treasury yields which do not reflect the real US inflation rate that folks such as shadowstats put as high as 10% against official CPI of 2.7%.

The bottom line is that the US is on an accelerating trend towards a dollar crash event when there is panic loss of confidence in dollars and by virtue of virtually every other currency will suffer to a great extent as all currencies are locked into a money printing death spiral towards oblivion, the only difference between currencies is the volatility in the differing rates of free fall which are the exchange rates that the financial press blandly reports on a daily basis.

Now, everyone’s apparently a dollar bear, though backtrack a few months to December 2010 with the USD Index breaking above 80 and the prevailing mood was turning decidedly bullish, with much talk in the financial press and blogosfear (ignoring dollar perma-bears) for the possibilities of USD rallying all the way to 90, which was not destined to happen as I commented upon at the time that it was a great time to load up with dollar shorts.

My long standing USD analysis (12 Oct 2010 – USD Index Trend Forecast Into Mid 2011, U.S. Dollar Collapse (Again)? ) concluded in the following trend expectation for the U.S. Dollar into mid 2011 in that it targets a mid 2011 low of around 69-70. Currently the USD index stands at 73 which puts the trend firmly inline with the forecast expectations of over 7 months ago.

Here are a couple of quick examples of mainstream financial press expectations for the US Dollar for 2011.

ABC News – 1st Jan 2011 – US Dollar Seen Rising in 2011 After Rough 2010

Never mind the lacklustre economy, the huge trade deficit or the government’s piles of debt: The U.S. dollar is still expected to outperform most of the world’s major currencies next year.

“By all rights, the dollar should be declining in value, but it’s not,” says Eswar Prasad, economics professor at Cornell University. “For the dollar to decline in value, you must have currencies on the other side that will” rise.

Bad as things are in the United States, they look worse in Europe and Japan, making the yen, the euro and the British pound riskier bets in 2011. A notable exception is the Chinese yuan, which is likely to rise next year as Beijing fights inflation.

“The dollar remains the ultimate safe haven,” Prasad said.

FT – 7th Jan 2011 – Dollar rally finds fresh impetus

Derek Halpenny at Bank of Tokyo-Mitsubishi UFJ said he expected the dollar to continue to outperform other main currencies regardless of the outcome of the employment report.

“Our stronger bias for the dollar in 2011 is based on a number of factors, all of which are likely to result in an outperformance of the US economy relative to other major countries or regions,” he said.

The Dollar’s trend trajectory remains for USD index to nudge below USD70 by mid 2011 (June), the original expectations were for the dollar to rally from the new low point, which still stands as the most probable outcome given that a fall below USD70 will trigger an avalanche of dollar collapse / hyperinflation crash / expectations. I will revisit expectations for the USD index in an in-depth analysis for the remainder of the year during June.

Events to Help Keep the Masses Sedated

Whilst many vocally denounce the Fed as it plays smoke and mirrors with economic data so as to manage the populations inflation and economic expectations. However the Fed is an amateur when compared against other much older institutions.

Several events during the week played their parts in keeping the masses sedated, In Britain, we had the Royal Wedding that was watched by near half the nation and many hundreds of millions more in former British colonies such as the United States, Canada and Australia.

The workers of Britain and the U.S. are being squeezed by higher taxes and falling pay in real terms courtesy of high real inflation, so there’s nothing like a FREE multi-national event to distract people from their economic plight.

Meanwhile the Vatican conjured a miracle out of its magic hat as the current Pope beatified the preceding pope in response to an apparent miracle of a nun cured of Parkinson’s (medical miss diagnoses?) following prayer to the preceding pope during 2005 (who suffered also from Parkinson’s). There’s nothing like the drug of a miracle that gives hope to millions of suffers and their families to fill church congregations and coffers, give the Fed a few hundred years and future Fed Chairmen will be similarly attired and held in just as much reverence as they announce the future miracle of QE free money.

Obama Killed Osama?

And lastly, the Sept 11th terrorist mastermind, Osama Bin Laden was apparently executed Sunday night (EST), coming as a surprise to many that he was still alive since many had concluded that he had probably died of kidney failure several years ago.

On the news, celebrations broke out across America and right from President Obama downwards calls were heard of justice being served. Though I find it strange that justice can be served without a trial?

Why Was Bin Laden’s Body So Quickly Buried at Sea?

The fact that his body was apparently quickly disposed of at sea smells very fishy to say the least. The whole event smells of a great stage managed propaganda piece that the mainstream media was more than happy to propagate. The facts are that an increasingly financially broke United States needs to withdraw from the costly Afghanistan occupation (as already announced by President Obama) and the primary reason for invading and occupying Afghanistan was to get Bin Laden, therefore it is timely for Bin Laden to be suddenly found, killed and quickly disposed of at sea therefore paving the way for the U.S. to say siagnora to Afghanistan, especially if the U.S. now has Iran in its sights hence a requirement to replenish and re-deploy military assets.

It may well be that Bin Laden had already died several years ago of kidney failure and it was in U.S. geopolitical interests to keep Bin Laden alive up until the decision to withdraw from Afghanistan. Skeptical ? Remember that the Iraq War that has cost upwards of 100,000 lives was undertaken under the basis of Bush and Blair lies.

As for President Obama, he played the ultimate patriot card Sunday night that no republican can match, a great way for him to start his re-election campaign with, as even republicans were singing his praises, given that there is speculation that the US has known of the compound for several years, perhaps the news breaking closer to the 10th anniversary of Sept 11th would have deemed to have been a little too suspicious.

Source and Comments: http://www.marketoracle.co.uk/Article27904.html

By Nadeem Walayat

Copyright © 2005-2011 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved.

Nadeem Walayat has over 25 years experience of trading derivatives, portfolio management and analysing the financial markets, including one of few who both anticipated and Beat the 1987 Crash. Nadeem’s forward looking analysis focuses on UK inflation, economy, interest rates and housing market. He is the author of three ebook’s – The Inf lation Mega-Trend; The Interest Rate Mega-Trend and The Stocks Stealth Bull Market Update 2011 that can be downloaded for Free.