Gold Fundamentals Not Bullish Yet

Ask a gold bull why Gold hasn’t performed well over the past 15 months, and you might hear the words manipulation, suppression, or Bitcoin in the response.

You won’t hear that Gold gained nearly 80% in two years and was historically overbought.

Last but not least, you won’t hear about the fundamental changes that have driven capital outflows from Gold and Silver, as well as bonds and into stocks and commodities.

Concerns about growth and Covid in 2020 dissipated as the market gained confidence in an economic recovery and the end of the deflation threat.

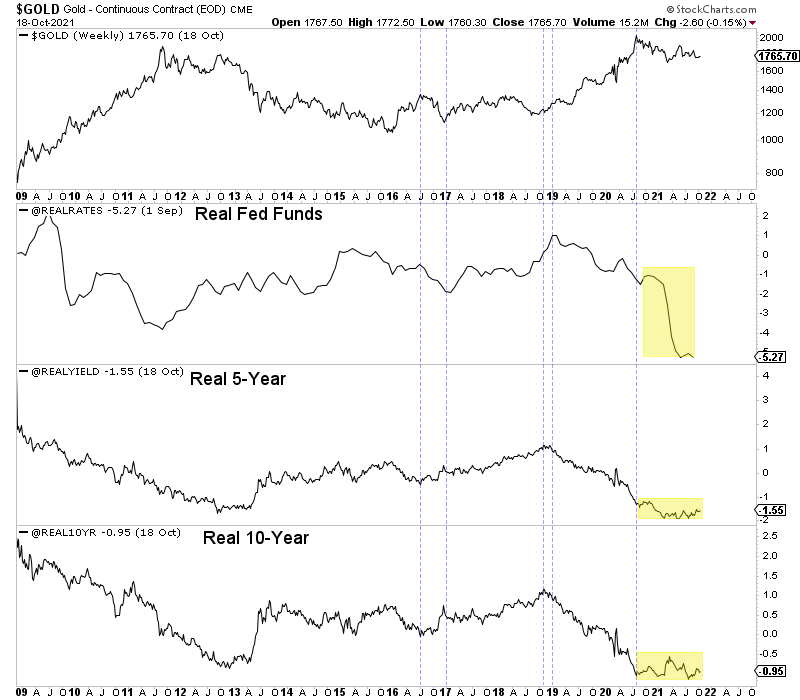

For Gold specifically, the problem is that real interest rates blew out to the downside (much like in 2011-2012, 2008, 1980, and 1975). As inflation moderates and yields rebound, real interest rates will rise, or at least not decline.

That is best illustrated by the real 5-year and real 10-year yields and not the real fed funds rate, which, at times, can lag.

At present, the market has started to discount that inflation will be sustained or sticky and not transitory.

One would think this is good for Gold, but the stock market is recovering again, and commodity prices (led by Oil and Copper) are making new highs. That combination reflects growth more so than inflation.

The narrative of growth and inflation, along with expectations of higher interest rates, has hurt Gold. When inflation persists for several quarters and begins to impact growth, the narrative will shift to stagflation and the associated problems from inflation. Then Gold is bullish.

A signal for that turning point could be the Fed starting rate hikes.

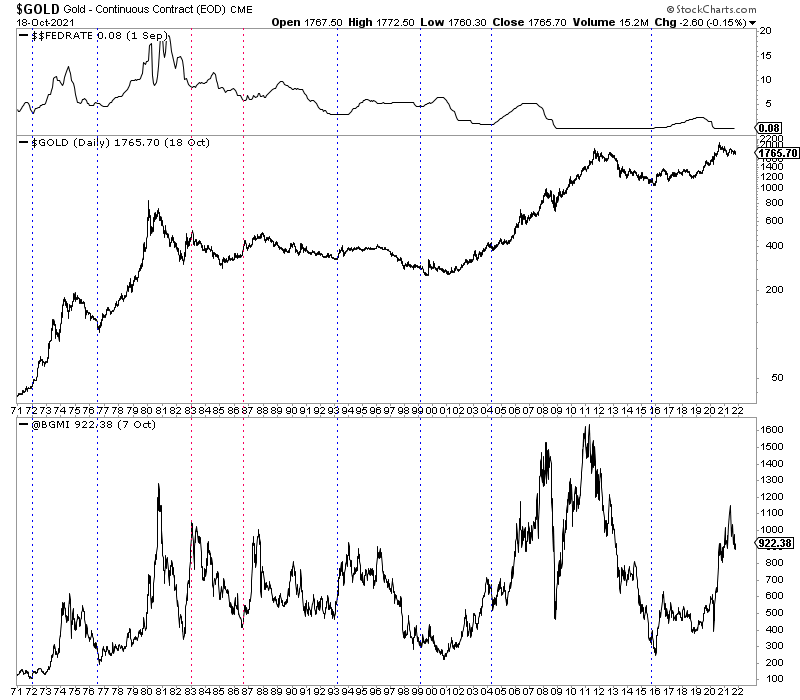

We plot the Fed Funds rate, Gold, and the Barron’s Gold Mining Index. The vertical lines mark the start of Fed rate hike cycles.

As you can see, the start of rate hikes is very bullish for Gold and gold stocks. The beginning of the last four rate hike cycles marked an average initial rebound in Gold of 27%.

Current fundamentals for Gold are not bullish, and that is reflected in recent price action. However, persistent inflation (a view which the market has started to adopt) will lead to bullish fundamentals in Gold.

The market discounts in advance, and the turning point could be when the Fed hikes interest rates. History shows this is usually a very bullish catalyst for Gold and gold stocks.

Expectations for a rate hike are surging. The market has priced in two hikes next year and is showing a 50-50 chance of a rate hike as soon as June 2022.

For now, I’m focused on finding quality juniors with 7 to 10 bagger potential over the next two to three years. The recent decline in the sector has priced out much of the risk in these stocks and enhanced the potential upside for new buyers.

In our premium service, we continue to identify and research those companies with considerable upside potential over the next 24 months. To learn the stocks we own and intend to buy, with at least 5x upside potential after this correction, consider learning more about our premium service.