Why Gold May Be Finally Turning Higher

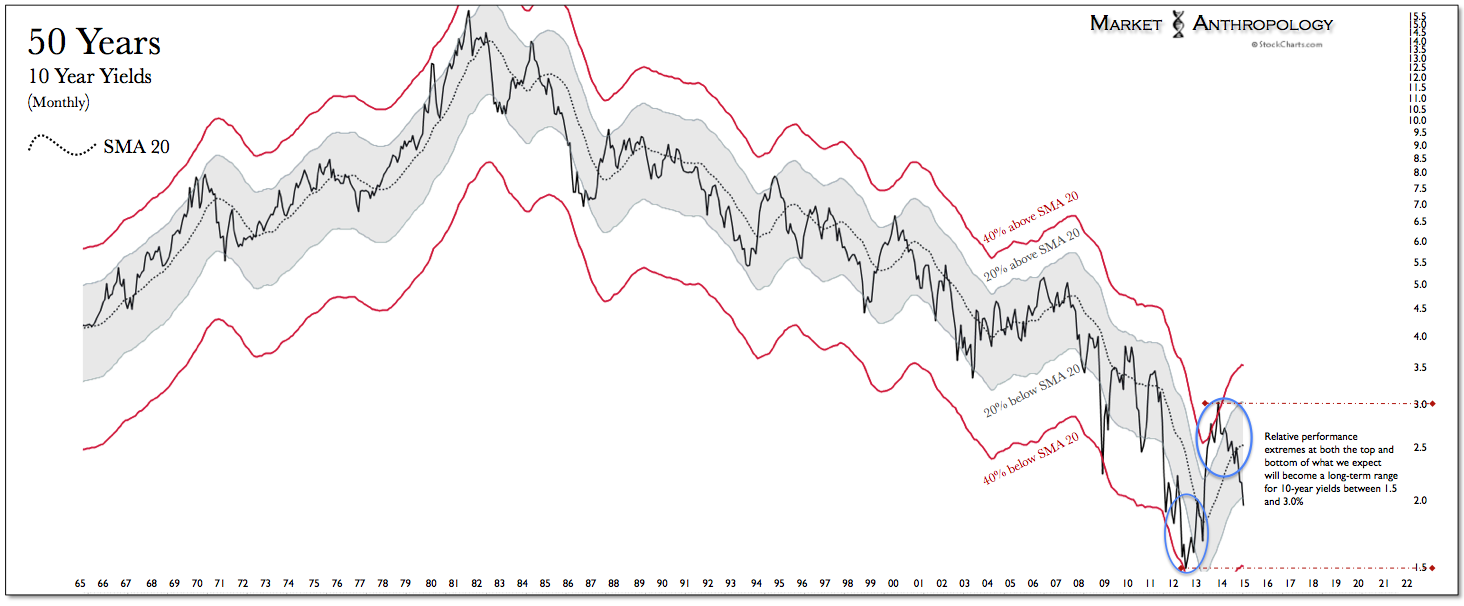

We came into last year with the idea that despite a historically low disposition at 3 percent, the 10-year yield had become stretched at a relative performance extreme. In less than two years, yields had run up over 100% above the July 2012 cycle lows around 1.4 percent. Even in context of previous rate tightening cycles, such as the one in 1994 that had caught the market offsides – the move was massive. When expressed on a logarithmic scale, the less than two year rip was the most extreme in over fifty years.

Click to enlarge images

Not surprisingly, when viewed in this light, our expectations going into last year were for 10-year yields to retrace a significant portion of the move; hence, strategically we favored long-term Treasuries relative to U.S equities, which by most conventional metrics as well as our own variant methods – were also extended. To guide the arc of those expectations, we referenced throughout the year the complete retracement profile of the 1994/1995 rate tightening cycle – as well as an inverse reflection of the secular peak in yields from 1981 that momentum was loosely replicating on the backside of the cycle.

With a year of daylight between that extreme, yields are still following both retracement profiles – with 10-year yields just today feathering the panic lows from last October. While respective retracements in both Treasuries and equities may manifest over the short-term, strategically speaking, we continue to favor Treasuries – considering that the U.S. equity markets remained relatively buoyant last year.