The Next Fundamental Catalyst for Gold

Amid the false breakout in the gold and silver miners and what appears to be the false breakout in Gold (above $1900), I want to step back and review the fundamental landscape.

Yes, inflation is raging, and that should be good for Gold. But not yet.

The reason is twofold: real interest rates stopped falling 12 months ago, and the economy has not yet hit stagflation.

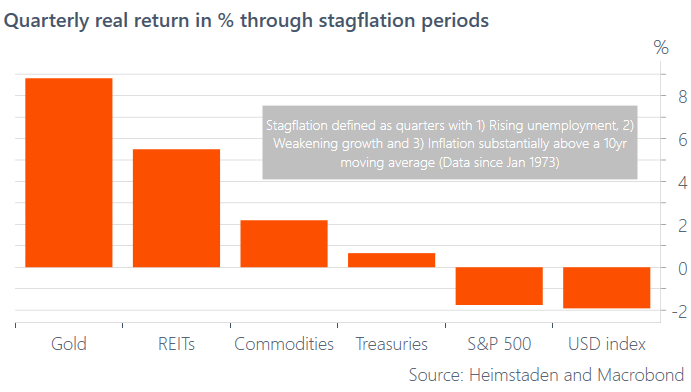

The inflationary environment best suited for Gold includes rising unemployment and weakening growth. The economy is still adding jobs and real GDP growth in the last five quarters was 4.5%, 6.3%, 6.7%, 2.3%, and 6.9%.

Growth at best is going to slow, and the market has discounted that as Gold rebounded in the first quarter, and the Gold to S&P 500 ratio is back above its 200-day moving average for the first time in 18 months.

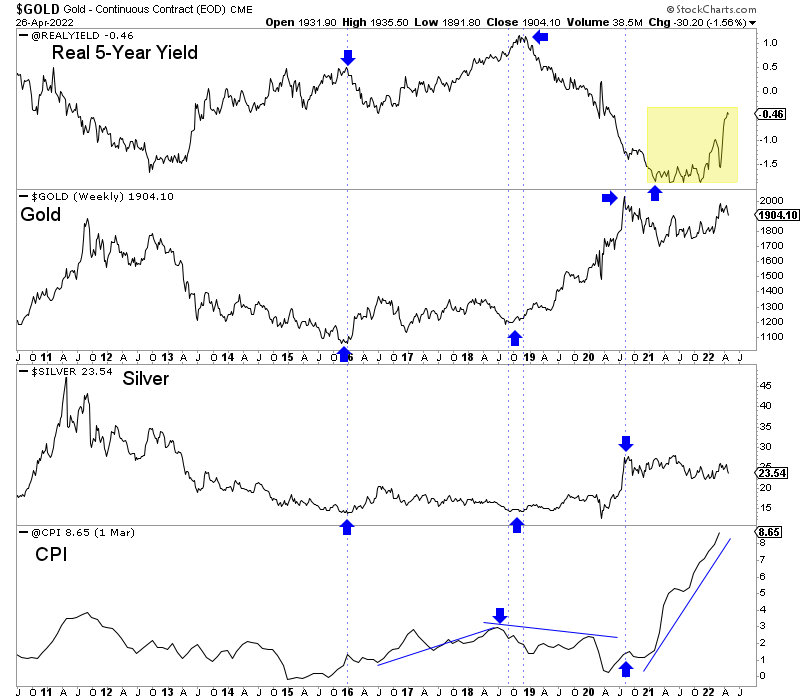

The main issue for Gold is real interest rates rising as the market discounts aggressive hikes from the Fed. Real interest rates bottomed a year ago and have risen even as the inflation rate increased from below 2% to 8.65%.

Since 2016 Gold and Silver have underperformed during rising inflation due mostly to rising real interest rates.

As we wrote three weeks ago, the catalyst for this correction to end and Gold to break $2,100 could be the market sniffing out the end of the Fed rate hike cycle.

That will coincide with the economy trending towards recession and inflation rolling over. And then you have true stagflation with declining or negative growth, unemployment turning up, and inflation (albeit falling) still a problem.

The window to buy quality juniors at cheap valuations reopened, but it will not be open for too long.

I continue to be laser-focused on finding quality juniors with at least 5 to 7 bagger potential over the next few years. To learn the stocks we own and intend to buy, with at least 5x upside potential after this correction, consider learning more about our premium service.