Understanding the Gold Cycle

Regular readers by now are familiar with Gold’s fundamental drivers and the influence of the stock market.

Falling and or negative real interest rates are the fundamental driver for Gold and are usually a byproduct of a weak stock market and economic recession.

However, today I want to focus on the larger cycle for Gold and at which points it performs and performs best. Secondly, perhaps more importantly, the Gold cycle has major implications for the gold miners.

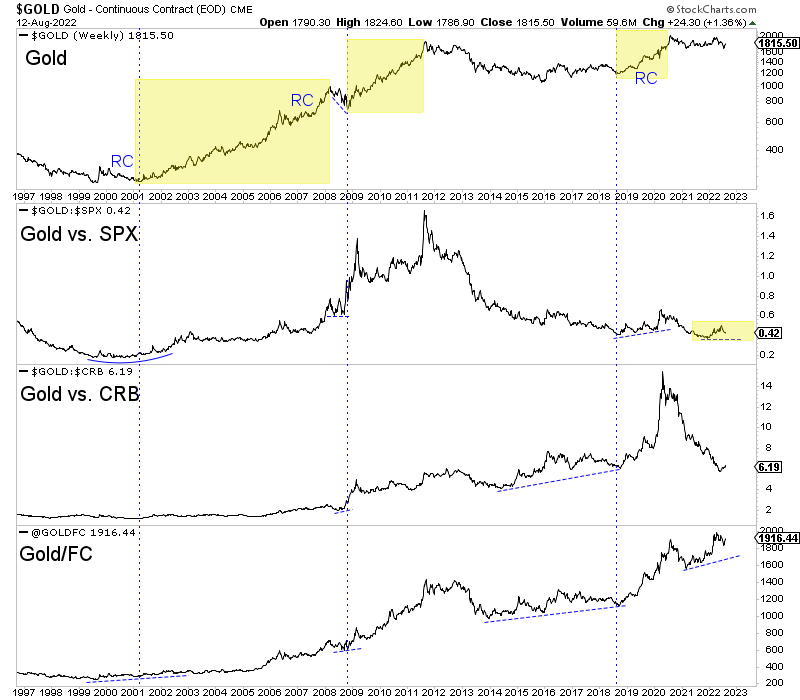

There have been three Gold cycles over the past few decades. Those were 2001 to 2007, 2008 to 2011, and 2018 to 2020.

The cycles revolve around bear markets in stocks and or recessions.

Usually, but not always, Gold will begin to outperform risk assets (stocks, commodities, currencies) during the downturn. This typically precedes strong nominal performance and also strong outperformance from the gold miners.

The turning point, in nominal terms, is around the time the Fed shifts policy and starts easing. The RC marks the first interest rate cut in that particular cycle.

In the current fledgling cycle, Gold is outperforming the stock market and has just started to outperform commodities.

The stock market will ultimately determine whether we get another full blown Gold cycle or not.

Further weakness in the stock market and the economy increases the odds of a shift in Fed policy. The worse the economy gets and the lower the stock market, the greater the odds of Fed rate cuts.

Gold’s biggest moves come during those shifts and, more importantly, gold miners’ biggest moves. That is the time when Gold is strongly outperforming miners’ input costs.

Gold starts to lose its fundamental luster when the economic expansion gains traction, commodity prices have rebounded, and the Fed can start raising rates.

Of course, this does not sum up every cycle, but you can understand the importance of economic weakness, Gold outperformance, and Fed policy changes.

This Fed cycle is an inflationary one and has required significant tightening. The difference between today and the Gold cycles of the 1970s, to this point, is today, we have yet to reach a full-blown recession and rising unemployment.

However, as in most scenarios, a recession and lower lows in the stock market will be the catalyst for the coming Gold cycle.

I continue to focus on finding high-quality juniors with at least 5 to 7 bagger potential over the next few years. To learn the stocks we own and intend to buy, with at least 5x upside potential after this correction, consider learning more about our premium service.